Tax avoidance

2026-07-03

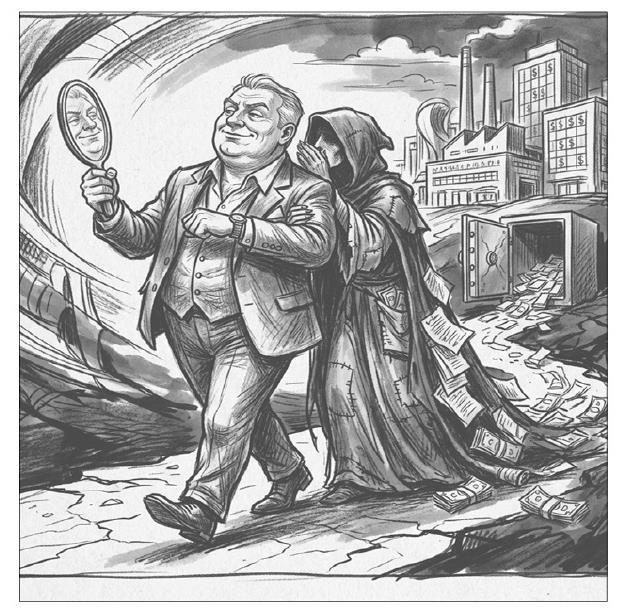

THER E has been a growing concern in the corporate world regarding the influence of CEO narcissism on an organisation`s sense of business ethics. In many organisations, leaders with excessive self-focus and overconfidence often prioritise personal image, profits and short-term gains over legaland ethicalresponsibilities.

Research regarding behavioural corporate finance indicates that CEOs with strong narcissistic tendencies, characterised by excessive self-confidence, dominanceand a heightened need for admiration, are more likely to engage in aggressive tax strategies. While such strategies may enhance short-term financial performance and personal reputation, they often come at the cost ofethicalresponsibility and legaltransparency.

Recent studies in corporate governance also suggest that narcissistic CEOs are more likely to engage in aggressive tax planning and exploit loopholes to minimise tax payments. While such actions may temporarily benefit firm earnings, they ultimately harm national revenue systems, reduce public resources and weaken trust in institutions.

In developing economies like Pakistan, where tax compliance is already a major challenge, such practices further deepen inequality and limit government capacity to invest in education, healthcare and infrastructure. This mal(es the issue notonly a corporate governance concern, but also a broader social and economic problem.

Regulatory bodies and tax authorities must strengthen monitoring systems and enforce strictercorporate transparency standards. At the same time, organisations should adopt better leadership selection processes that consider ethical behaviour and psychological traits, not just financial performance.

Addressing this crucial issue is essential for building a fair, transparent, effective and accountable corporate environment that supports overal national development.

R afia Rafique Ahmed Panhwar Dadu